Texas car accident insurance claims revolve around four main issues: fault, coverage, damages, and proof. In most cases, the driver responsible for the crash must pay for the harm, usually through that driver’s liability insurer. However, other types of coverage—such as PIP, collision, health insurance, or uninsured motorist benefits—may also apply in certain situations.

Each issue is reviewed individually. First, our car accident lawyer in Houston determines who caused the crash. Next, we identify every policy that might pay. Then, we measure the full loss. Finally, we gather evidence linking the crash to injuries, lost income, and vehicle damage. By using this step-by-step method, we help prevent key coverage from being missed.

Texas Uses an At-Fault Car Insurance System

Texas uses an at-fault system for car crashes. A driver who causes a wreck may be liable for the resulting harm. That harm may include medical bills, lost income, car damage, pain, impairment, and scars. Liability insurance pays covered claims against the insured driver. Payment is limited by the policy limits.

Fault is not based only on a ticket or an apology. We look at the full record. Useful proof may include the crash report, photos, video, witness statements, and vehicle damage. Serious cases may also require phone records, black box data, or an accident expert.

Who Pays After a Texas Car Accident

The At-Fault Driver’s Liability Insurance

When another driver causes a crash, that driver’s liability policy is usually the first source of payment. Bodily injury coverage covers injury losses, and property damage coverage covers vehicle and other property damage. The insurer may also pay toward towing, storage, and rental costs.

The insurer will not pay just because a claim was opened. It will study faults, coverage, injuries, and damages. It may be argued that both drivers were at fault. It may also dispute whether the crash caused all the treatment. Strong proof is needed before serious settlement talks begin.

The Injured Person’s Own Auto Insurance

A person’s own policy can pay some benefits sooner. PIP may pay covered medical bills and lost income. Collision coverage pays to repair or replace the insured car. A deductible usually applies to a collision claim. UM or UIM coverage may apply when the other driver has no insurance or too little insurance.

Using your own policy does not mean you caused the crash. You are using coverage you bought for this risk. Your insurer may later seek repayment from the other driver’s insurer. This subrogation may recover all or part of your deductible if sufficient funds are recovered.

Other Responsible Parties and Policies

Some crashes involve more than one person or policy. An employer may be liable when an employee causes a crash while performing job duties. A rideshare or delivery company may provide coverage based on the driver’s app status. A vehicle owner’s policy may apply when someone else drives with permission.

Other claims may involve a bar, a repair shop, a parts maker, or a road contractor. These claims depend on the facts. Finding every policy matters. One minimum policy may not cover a surgery, a long hospital stays, or several injured people.

Texas Minimum Auto Insurance Limits

Most Texas drivers meet the state’s financial responsibility requirements by purchasing liability insurance, typically with minimum limits of 30/60/25. This means the policy pays up to $30,000 for injury to one person, up to $60,000 total for injuries to two or more people, and up to $25,000 for property damage in a single crash.

The current limits are set out in Texas Transportation Code Section 601.191.

These limits are often too low. Newer vehicles can exceed $25,000 in value, and a multi-car crash can split that limit among several owners. The $30,000 injury limit is quickly exhausted with ambulance, scans, surgery, and time off work.

Types of Car Insurance Coverage in Texas

A Texas auto policy can include several types of coverage, with each providing a distinct purpose. The declaration page lists coverage, limits, deductibles, cars, and named insureds. To avoid surprises, we review the full policy and all endorsements, since an insurance card alone does not reveal every term.

| Coverage | Who It Protects | What It May Pay |

| Liability | Other people when the insured caused the crash | Injury losses, car damage, and related costs up to the limits |

| Collision | The insured car | Repair cost or actual cash value, less the deductible |

| Comprehensive | The insured car | Theft, flood, hail, fire, vandalism, and other non-crash losses |

| PIP | The insured and other covered people | Covered medical bills, lost income, and some other costs |

| Medical Payments | The insured and covered passengers | Covered medical and funeral bills |

| UM or UIM | The insured and other covered people | Losses caused by an uninsured, underinsured, or hit-and-run driver |

| Rental Reimbursement | The policyholder | A daily amount for a rental or other travel |

| Gap Coverage | The borrower or lender interest | Part of the gap between a total loss payment and the loan balance |

Liability Coverage

Liability coverage protects the insured against claims by others, not the insured’s own losses. Bodily injury coverage may pay medical costs, lost income, pain, impairment, and scars. Property coverage may pay for repair, total loss, towing, storage, and loss of use.

Collision and Comprehensive Coverage

Collision coverage pays for damage to the insured car after a crash. It can apply even when the insured caused the wreck. A deductible usually applies. Comprehensive coverage pays for many losses that are not caused by a crash. Common examples include theft, flood, hail, fire, vandalism, and an animal strike.

Personal Injury Protection

Texas auto policies generally include at least $2,500 in PIP. A named insured can reject it, but the rejection must be in writing. Higher limits may be offered. PIP may pay covered medical bills, lost income, and some other costs. It can pay without proof that another driver was at fault.

The PIP offer and written rejection rules are set forth in Texas Insurance Code Sections 1952.151 and 1952.152.

Medical Payments Coverage

Medical payments coverage can pay medical and funeral bills for covered people, but it is not the same as PIP. Unlike PIP, MedPay usually does not include the same wage loss benefits. Sometimes, the policy also gives the insurer the right to seek repayment. Before a settlement is signed, we review those terms.

Uninsured and Underinsured Motorist Coverage

Texas insurers must offer UM and UIM coverage. A named insured must reject it in writing to remove it.UM coverage applies when the at-fault driver has no insurance. UIM coverage applies when that driver has insurance, but the limits are too low. Coverage may also apply after a hit-and-run crash.

The written rejection rule appears in Texas Insurance Code Section 1952.101. Standard Texas UM property coverage has a $250 deductible.

Rental Reimbursement and Gap Coverage

After a covered loss, rental reimbursement pays a set daily amount, and the policy also defines a total limit. By contrast, gap coverage serves a different purpose: following a total loss, it may pay part of the difference between the car’s value and the loan balance. However, gap coverage does not increase the car’s value or pay for injury damages.

How Fault Is Proven in a Texas Car Accident Claim

A claim must be supported by verifiable proof of fault. We begin with photos, vehicle damage, road marks, traffic signs, and witness information, then proceed to review police reports and medical records. Sometimes, video from a store, home, dash camera, or traffic system gives vital insight into the crash.

The police report is useful, but it is not always final. Sometimes, the officer arrives after the cars have moved or may not have access to later video or data. By comparing the report with all other proof, we help secure accuracy. Fast action matters because video can be erased and cars can be repaired or sold.

Texas Comparative Responsibility Can Reduce Recovery

Texas applies a modified fault rule: if a claimant is more than 50 percent at fault, they cannot recover damages. However, if the claimant’s fault is 50 percent or less, recovery is allowed, but the award is reduced by that same percentage. For example, a $100,000 loss becomes $80,000 when the claimant carries 20 percent of the fault.

This rule appears in Texas Civil Practice and Remedies Code Section 33.001.

Adjusters often raise the issue of shared fault early in the process, focusing on elements such as speed, lookout, lane use, turns, or following distance. We insist on proof before accepting any assigned percentage; the claim record must show what each driver did and whether their conduct contributed to the crash.

First Party and Third-Party Claims Are Different

When you make a first-party claim, you do so under your own policy. Common examples include PIP, collision, rental, and UM/UIM claims. Because you have a contract with your insurer, the policy sets duties for both sides. While you must give notice, furnish the necessary records, and meet the policy terms, the insurer must review the claim under the policy and under Texas law.

A third-party claim is filed against the other driver’s liability policy. Unlike with your own insurer, you do not have contract rights with that insurer. This distinction matters when the carrier is waiting for its driver to answer calls or when the carrier refuses to accept fault.

Texas prompt payment deadlines for first-party claims do not apply in the same way to the other driver’s insurer. A low offer or delay is also not always a direct bad-faith claim. Rights and remedies depend on who bought the policy, the type of claim, and the insurer’s conduct.

Texas Insurance Claim Deadlines

For many first-party claims, an insurer must act within set time periods. It generally has 15 days to confirm the claim, begin its review, and request any needed items. After it gets the needed items, it generally has 15 business days to accept or reject the claim. It may take up to 45 more days if it gives a reason. An accepted claim is generally due within five business days.

These rules are explained in the Texas Department of Insurance auto insurance guide and Texas Insurance Code Chapter 542.

The policyholder must still assist with the claim by providing photos, estimates, medical records, or proof of loss, if requested. We keep a claim log that should list every call, email, request, and response. By keeping this record, we can show when the insurer had enough information to decide the claim.

Finally, resolving property damage after a car accident in Texas brings its own steps and choices, especially concerning vehicle repairs.

Although an insurer may recommend a repair shop, the owner usually selects one. Sometimes the initial estimate overlooks hidden damage, and the shop may request a supplement after the car is disassembled. Take clear photos of every side of the car before repairs begin. In addition, be sure to save records for towing, storage, and rental.

Disputes may involve labor rates, parts, paint work, or safety system calibration. The insurer may use parts of like kind and quality instead of factory parts. The repair scheme should make the car safe. A low estimate should not control when the shop finds more crash damage.

Rental Car and Loss of Use

The at-fault driver’s insurer may owe a rental car or loss of use. Payment usually lasts for a fair repair period. If the car is totaled, the rental payment may end soon after the carrier gives notice. Parts delays and added damage should be reported in writing.

Your own insurer pays rental costs only when the policy provides that benefit. Rental coverage has daily and total limits. UM property coverage may also pay rental costs in some cases. The declaration page should be checked at the start of the claim.

Total Loss Value

A carrier may total a car when the repair cost is near or above its value. Some carriers use a lower point. The payment is based on the car’s value before the crash. It is not based on the loan balance. It is also not based on the price of a new replacement car.

Mileage, trim, options, condition, and local sale prices can change the value. Recent tires or major service may also matter. A weak-value report may include cars with the wrong trim or mileage. We compare each listed car and point out errors.

The Texas Department of Insurance total loss guide suggests using local dealer quotes and similar cars to challenge a low value.

An owner may choose to keep the salvage. The carrier will then subtract salvage value. Title rules may also apply. A borrower may still owe money after the total loss payment. Gap coverage may help if it was bought before the crash.

Diminished Value

A repaired car may still sell for less because of its crash history. Texas allows diminished-value claims in some third-party and UM property claims. Proof should compare the value before the crash with the value after repair. The damage level, repair quality, and local market all matter. A sound appraisal is better than a simple online formula.

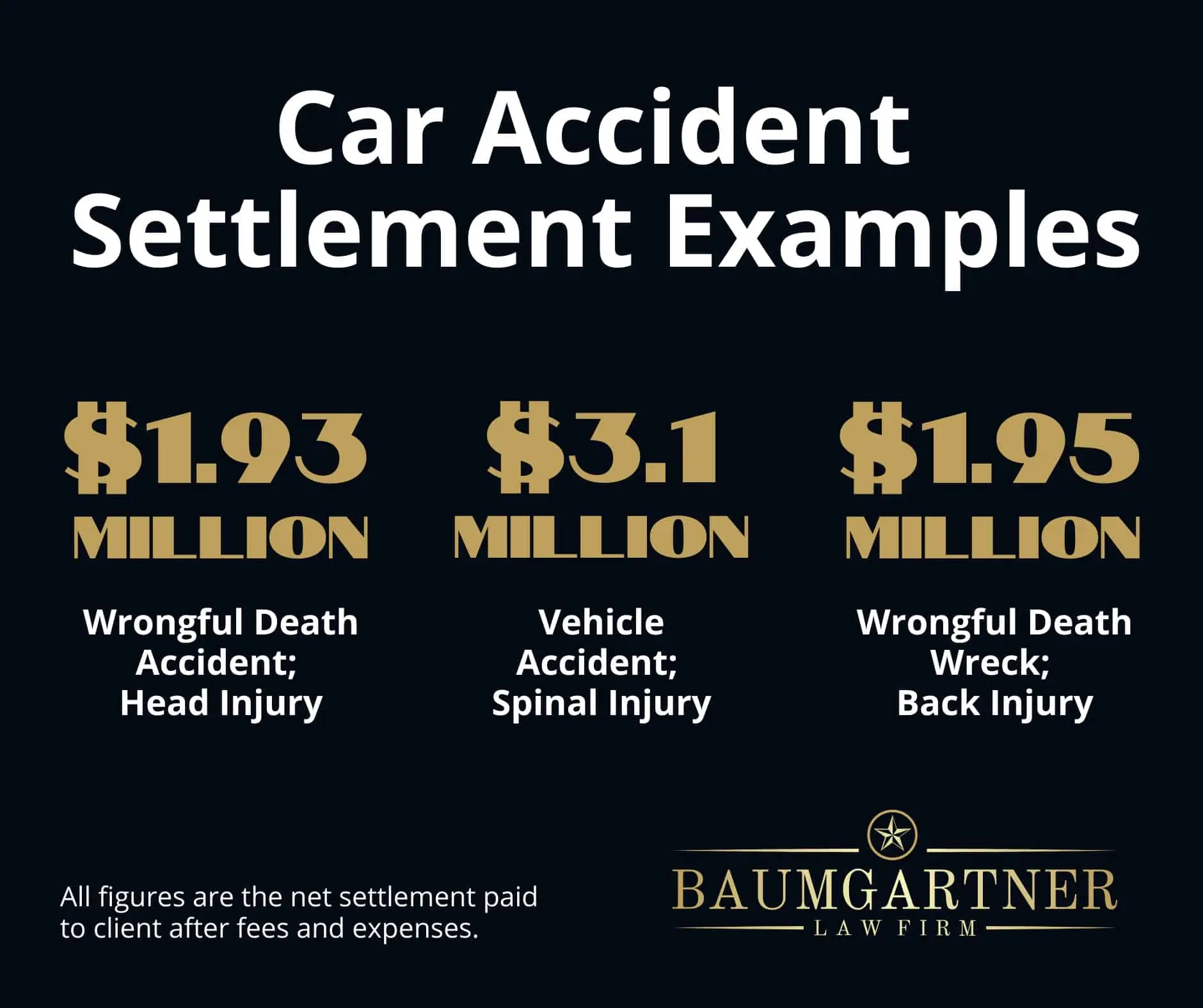

Damages in a Texas Car Accident Injury Claim

There is no fixed formula for the value of an injury claim. at Baumgartner Law Firm we measure the actual harm. We also gather proof for each part of the loss. The injury, treatment, work impact, future care, fault, and available insurance all affect value.

Medical Bills and Future Care

Medical damages may include ambulance transport, emergency treatment, scans, doctor visits, therapy, injections, surgery, medication, and rehab. Future care must be likely and tied to the crash. A doctor may need to explain the treatment plan, cost, and expected results.

Insurers study the need for care and the amount charged. They may point to missed visits, gaps in care, or an old injury. An old condition does not always defeat the claim. A driver can be liable for worsening an existing problem. Medical records should show the person’s condition before and after the crash.

Lost Income and Reduced Earning Power

A claim may include missed pay, lost overtime, used leave, and lost bonuses. It may also include reduced future earning power. Pay records, tax returns, employer letters, and work limits help prove the loss. A self-employed person may need invoices, contracts, and business records.

Pain, Mental Anguish, Impairment, and Scars

Texas law allows payment for personal harm that is not shown on a bill. Physical pain refers to the pain caused by an injury. Mental anguish covers deep emotional suffering. Impairment covers the loss of daily activities apart from pain. Disfigurement covers lasting changes in appearance. Photos, records, and witness accounts can show these losses.

Property Loss and Other Costs

A full claim may include the car, damaged items, towing, storage, rental costs, and trips to care. It may also include help with the home or alterations required for a disability. Save receipts when possible. Photos, estimates, calendars, and witness statements can also serve as evidence of the expense.

Health Insurance, Medical Liens, and Repayment Claims

The at-fault driver’s insurer usually does not pay medical bills as care happens. It often waits until the injury claim can be valued. PIP, MedPay, health insurance, Medicare, Medicaid, or workers’ compensation may pay first. Some doctors may also wait to be paid from a settlement.

These payments can create liens or repayment claims. A health plan, government program, hospital, or workers’ compensation carrier may claim part of the settlement. Each claim should be checked. The amount on a bill is not always the amount that must be repaid. Final balances and valid lien papers are required before funds are sent.

A settlement should be judged by the net amount. Fees, case costs, medical balances, and repayment claims reduce the amount the client receives. A large gross offer may be poor if the unpaid costs are also large.

Uninsured Drivers, Underinsured Drivers, and Hit-and-Run Claims

UM and UIM coverage can be vital in Texas. It may apply when the at-fault driver has no insurance or low limits. It may also apply when a hit-and-run driver cannot be found. Coverage may protect the named insured, family members, passengers, and other covered people.

A UIM claim is not automatic. The insured must still prove the other driver’s fault and the full extent of the damages. The UIM insurer may dispute fault, injury, value, or coverage. The claim is made under the insured’s own policy, but it still needs a strong case against the other driver.

Report a hit-and-run to police and the insurer at once. Take photos of damage, debris, paint marks, and the area. Ask nearby homes and stores about video. A quick report makes it easier to prove that another vehicle caused the loss.

Commercial, Rideshare, Delivery, and Borrowed-Vehicle Crashes

Personal auto policies may limit coverage during rideshare, delivery, or business use. Coverage may change based on the driver’s app status. A personal policy may apply when the driver is offline. Platform coverage may apply when the app is on, or a trip is active. Delivery cases can raise the same issue.

When a person borrows a car with permission, the owner’s policy is often the first source of liability coverage. The driver’s policy may provide added coverage. The result can change due to an excluded driver, a household rule, or a regular-use rule. We confirm who owned the car, who gave permission, and why the car was being used.

Commercial crashes may involve a company, a driver, a repair vendor, or another business. These cases may have higher limits and more records. Work logs, safety files, vehicle data, and company messages can be lost. Early preservation letters are important after a crash involving a truck, bus, van, or company car.

Common Insurance Tactics That Lower Claim Value

Insurance adjusters work for the insurance company. Their job includes testing for faults and limiting payment. A calm and complete response is more useful than an angry one. The injured person should still understand why the adjuster asks for each item.

· Seeking a recorded statement before the facts and injuries are clear

· Asking for broad medical releases that reach unrelated records

· Using a gap in care to argue that the injury was minor

· Relying on a low repair estimate before hidden damage is found

· Assigning shared fault without enough proof

· Offering quick money before future care and wage loss are known

· Using old injuries to deny that the crash made the condition worse

We answer these points with proof. A well-defined timeline, full records, wage papers, photos, and expert opinions can support the claim. Good records also make it harder to defend unfair cuts.

Recorded Statements and Medical Releases

An insured usually has a duty to help with a claim under the person’s own policy. That may include giving facts about the crash. Still, the timing and scope of a recorded statement matter. A person in pain, on medicine, or unsure of details may make an honest mistake. The insurer may use that mistake later.

The other driver’s insurer may ask for a recorded statement. The injured person usually has no contract duty to give one. A short factual talk may help with a simple car claim. A serious injury case requires greater care. Broad medical releases may also reach years of private records. We prefer records that are tied to the injuries and prior conditions at issue.

Settlement Offers, Policy Limits, and Releases

A settlement is final after the release is signed. The release often ends all claims arising from the crash. This can include an injury that gets worse later. Before signing, the injured person should know the diagnosis, likely recovery, future care, work limits, liens, and all available policies.

A policy limit caps what the policy must pay. It does not always cap the legal value of the case. The person or business may still owe more. Other policies or defendants may also exist. In a crash with many injured people, they may all seek payment from the same accident limit.

A good demand tells the story with proof. It explains fault, injuries, care, work loss, and daily limits. It also answers likely defenses. A stack of bills is not enough. The records should show how the crash changed the person’s health, work, and daily life.

When a Texas Car Accident Lawsuit Becomes Necessary

Many claims settle without suit. A lawsuit may be needed when the insurer denies fault or makes a very low offer. It may also be needed when key records are withheld. Suit allows formal requests for testimony, documents, phone data, vehicle data, and expert review.

A lawsuit puts the final choice in the hands of a judge or jury. It also brings cost, time, and risk. The choice should be based on the proof, amount at issue, coverage, assets, deadlines, and client goals. Trial readiness can improve settlement talks because the insurer must consider the risk of a verdict.

The Texas Two-Year Filing Deadline

Texas generally gives two years to file a lawsuit for injuries or property damage resulting from a car accident. The period usually starts on the crash date. Limited exceptions may apply, but they should not be assumed. An open claim or ongoing talks do not, by themselves, delay the deadline.

The general rule appears in Texas Civil Practice and Remedies Code Section 16.003. A claim against a government body may require much earlier notice.

Waiting can also hurt the proof. The video may be erased. Cars may be repaired or sold. Records may be lost. Witnesses may move or forget details. Early work protects the claim even when settlement talks take many months.

Steps That Protect a Texas Car Accident Insurance Claim

1. Call for emergency help when anyone may be hurt.

2. Call the police after an injury crash, hit-and-run, suspected drunk driving, or serious fault dispute.

3. Take photos of the cars, road, signs, debris, injuries, plates, and insurance cards.

4. Get names and contact details for independent witnesses.

5. Seek medical care soon and describe symptoms in a clear and honest way.

6. Report the crash to the proper insurers and save all claim details.

7. Keep damaged items, photos, bills, medical records, pay records, and a symptom calendar.

8. Check the policy for PIP, MedPay, collision, rental, UM or UIM, and umbrella coverage.

9. Do not sign a broad release before injuries, liens, losses, and coverage are reviewed.

10. Track the two-year deadline and any shorter notice rule that may apply.

A Complete Insurance Review Leads to a Stronger Claim

The key issue after a Texas car crash is not only whether the other driver has insurance, but also whether the driver is at fault. A fair result requires proof of fault, every policy that applies, and the full loss. It also requires quick action to preserve evidence and comply with policy requirements.

Our auto accident lawyer handles the claim as a series of definite steps. We find out who caused the crash. We identify the coverage. We prove the injuries and money losses. We then decide whether talks or a lawsuit offer the best path. This method gives the injured person a clearer view of the case and the likely net result.